王冠亚

· 湖北

巴菲特致股东的信原文精读Day797:

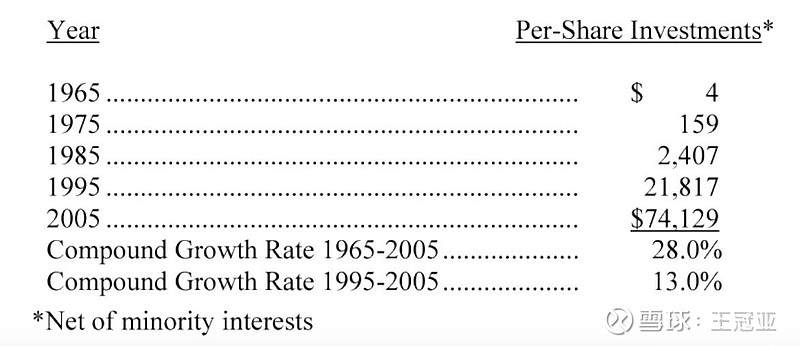

原文:Let’s review two sets of figures that show where we’ve come from and where we are now. The first set is the amount of investments (including cash and cash-equivalents) we own on a per-share basis. In making this calculation, we exclude investments held in our finance operation because these are largely offset by borrowings:

(2005)

释义:1.“equivalents”意为“等价物”;

2.“offset”意为“抵消”。

精译

点击查看全文