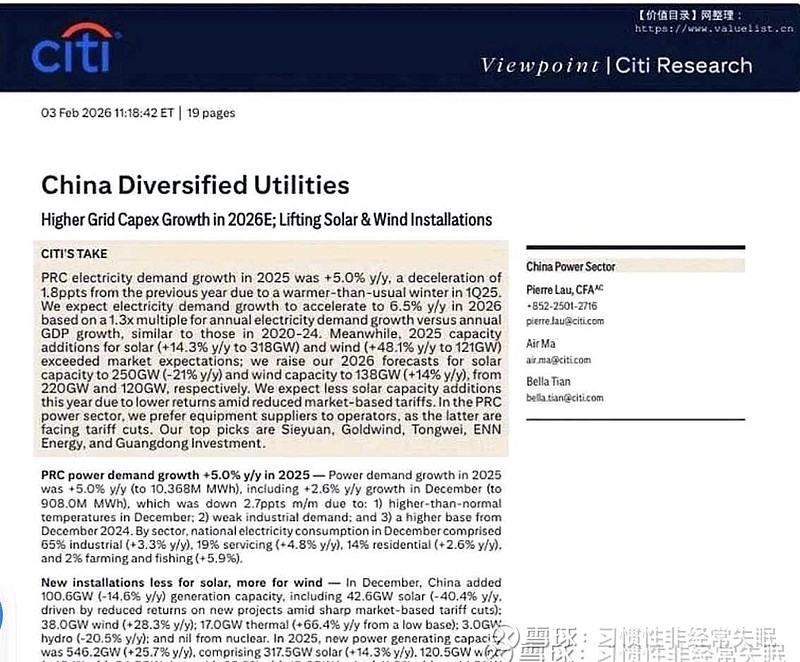

$思源电气(SZ002028)$超级电容获大众汽车定点,第三曲线已经出现。 作为长期持有者,经历过无数次波动,历经劫波思源在,相逢一笑260。

一、研报原文(思源电气专项分析)

Sieyuan Electric: Buy, Target Price RMB 260 (~40% Upside)

Sieyuan is our top pick in power equipment, benefiting from accelerating

domestic grid capex and tight global supply of high-voltage equipment,

especially in North America and the Middle East. Its overseas revenue mix

has improved materially, with orders from the U.S., Saudi Arabia, and Europe

growing rapidly.

We highlight its automotive electronics breakthrough: subsidiary GMCC has

secured formal qualification for Volkswagen’s new vehicle platform for

automotive-grade supercapacitors (start-stop systems and brake energy

recovery), with mass production scheduled for Q3 2026. This opens a new

long-term growth driver beyond grid and energy storage.

The 53% target price upgrade (from RMB 170 to RMB 260) reflects: (1) 2025

results beat consensus (revenue +37% YoY, net profit +54% YoY); (2) stronger

global transformer demand; (3) GMCC’s Volkswagen nomination; (4) proven

execution in overseas expansion.

We expect 2026E net profit growth of ~40%, supported by capacity expansion

in Saudi Arabia, Mexico, and Hungary.

二、精准中文翻译(投行研报正式版)

思源电气:买入评级,目标价260元(约40%上涨空间)

思源电气是我们在电力设备板块的首选标的,将直接受益于国内电网投资提速和全

球高压设备供给紧张(尤其是北美与中东市场)。公司海外收入结构已显著优化,

来自美国、沙特、欧洲的订单正快速增长。

我们重点关注其汽车电子业务突破:子公司烯晶碳能(GMCC)的车规级超级电容已

正式获得大众集团全新车型平台定点(用于启停系统与制动能量回收),计划于2026

年第三季度量产。这为公司在电网、储能之外,打开了全新的长期增长引擎。

本次目标价从170元上调53%至260元,核心依据包括:(1)2025年业绩超市

场预期(收入同比+ 37%,净利润同比+ 54%);(2)全球变压器需求持续走强;

(3)GMCC获得大众定点认证;(4)海外拓展执行力已被验证。

依托沙特、墨西哥、匈牙利的产能扩张,我们预计公司2026年净利润将增长约

4